The Hamiltonian and exactly where it comes from

Constrained optimization

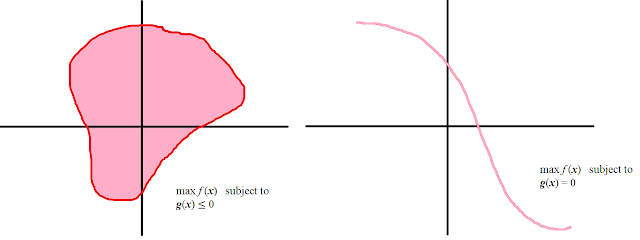

Suppose you wanted to optimize a function subject to some constraints (i.e. on a subset of ℝn) – so on something like the pink domains below:

If the optimal point x* lies within the interior of a domain like g(x) ≤ 0, then we have the gradient f′(x*) = 0 as usual – however, if the point lies on the boundary, then we could still be able to increase f by going outside the boundary, and still call x* an optimal point, as such points lie outside the domain. But we must have that f′(x) must point precisely outward normal from the boundary, otherwise we can find a directional derivative within the region to increase f in.

So we have f′(x) = λg′(x) for some λ ≥ 0 (with equality if – but not only if – x lies in the interior). And we also have the reverse implication if f and g are convex (why do they need convexity?). For equality constraints, we have the same constraint but don't need λ ≥ 0 (why?).

/But this is equivalent to optimizing/ the function f(x) − λg(x) – for some λ.

This function L(x,λ) is called the Lagrangian.

Duality